An Exposé Probing Legal Implications – Twitter & Elon Musk …the Real Story (Published April 11, 2022)

4/13 Update: Now a Class Action Lawsuit

The World’s Wealthiest Man (WWM) splashed again into the news cycle. This time, WWM revealed that he purchased a massive 9% plus stake in Twitter, making him temporarily the largest single shareholder of the giant social platform until Vanguard group reported a 10.29% position on Friday, April 8. With the acquisition, WWM sent news media buzzing with commentary. However, the significant legal and social implications of WWM’s actions have yet to be fully explored and understood. Until now.

• How WWM damaged marketplace trading for between $2.7B to $4.5B of Twitter securities. Not counting options market damage.

• How WWM openly purchased over 15 million shares of stock in a willfully skewed market of his creation and gained an astounding $165M additional net worth from those shares.

Let’s start with the most rudimentary functions of our public market. Our public markets exist for two primary reasons. First, to provide a venue for companies to raise capital for growing a business. Second, to provide a way for the public to invest in companies and share profits through dividends or stock appreciation.

Next, let’s briefly focus on the Securities and Exchange Commission (SEC). This independent Federal Government oversight agency’s mission is to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation. The goal is to better the economy and secure investors’ financial futures. The SEC provides a vital function for the Republic, and its fundamental institutional task falls on a little over 4,500 Full-Time equivalent employees.

While the SEC has extensive investigative and enforcement powers, it cannot file criminal charges. Hence, it can, and does, work with the Department of Justice (DOJ) to bring those charges. One example of this collaborative activity is the Foreign Corrupt Practices Act (FCPA) of 1977, which prohibits U.S. citizens, and entities from bribing foreign government officials to benefit their business interests. In this case, the DOJ handles criminal and civil penalties related to the actual act of bribery, while the SEC handles civil enforcement of violations of the FCPA’s accounting provisions.

So how does WWM fit in this picture?

WWM is many things depending on one’s point of view. Many supporters say he is a “revolutionary, fearless leader, visionary, entrepreneur, technocrat, and champion of free speech.” WWM refers to himself as a Technoking in his SEC disclosures. WWM also projects himself as a righteous rebel regarding his relationship with the SEC.

However, WWM belittles rules and creates controversy while acting in self-interest to gain favor for his companies. Like a class clown, WWM grandstands opportunities to show them up. WWM knows that his followers love it, hamming it up for his Twitter mob to gain greater social influence. All to be the “COOL” kid, one of the “BRUHS.”

Yawn. It is an old, boring act.

While WWM may inspire and sometimes be a catalyst for positive changes, that is no excuse to discount his actions and crude, crass comments.

Diving into WWM’s historical interactions with the SEC, in September 2018, the SEC charged WWM with securities fraud for false and misleading tweets about a potential transaction to take Tesla private. The implied deal WWM tweeted about never happened. WWM and Tesla agreed to a settlement with the government where WWM and Tesla would each pay a $20 million fine to the SEC. Additionally, WWM had to step down as the chair of Tesla’s Board.

Later, in June 2020, the SEC said WWM violated the agreement terms, which required WWM to have Tesla lawyers review any social media posts containing information “material” to shareholders and likely to affect the share price.

Then this year, the Tesla Annual Report for 2021, year-end, disclosed, “More recently, on November 16, 2021, the SEC issued a subpoena to us seeking information on our governance processes around compliance with the SEC settlement, as amended.” This SEC subpoena of WWM and Tesla following a poll of his tens of millions of Twitter followers, proposing he sell 10% of his Tesla stock.

WWM’s public taunts and frays with SEC regulators are antagonistic and sometimes obscene. In October 2018, WWM called the SEC the “shortseller enrichment commission.” Then, in July 2020, he posted, “SEC, three letter acronym, middle word is Elon’s.” Imbuing his idealogues’ inference instincts to think of a word starting with “S” and rhyming with “Duck” and the last word starting with “C” and rhyming with “Clock.”

On Monday, April 4, WWM filed the wrong form with the SEC regarding his Twitter stock purchases. Instead of form 13D, WWM filed as 13G. The difference being 13G is for passive investors with no intention of being active in the company. Often large funds use 13G filings. Considering WWM became a Twitter Board member the following day, April 5, and began aggressively advocating for changes, how and why did he file the 13G document?

Worse, the filing was late. Whether this was intentional or not is unknown.

Now, on April 10, at 11:13 PM, a posting from Twitter CEO Parag Agrawal stated:

“We announced on Tuesday that Elon would be appointed to the Board contingent on a background check and formal acceptance. Elon’s appointment to the board was to become officially effective 4/9, but Elon shared that same morning that he will no longer be joining the board.”

Let’s thoroughly examine the more significant issue of his actions’ implications.

Manipulative Trading, Power, Fair Markets

Given SEC’s mission to maintain fair markets, they codify and enact rules that all market participants must abide by, including WWM. Otherwise, some participants would take advantage of secret knowledge and power through financial means or other measures to game the system. And that is what WWM did and continues to do. WWM is no champion of the Republic even though WWM claims to be.

Transparency

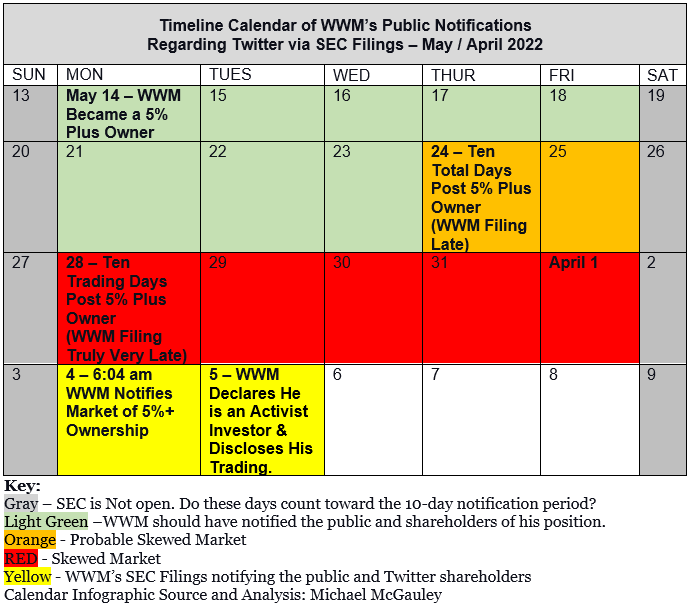

One requirement the SEC enforces is that 5% plus owners of public corporations must notify the market in a timely manner, defined as 10 days after acquiring more than 5% of the outstanding shares. It is not clear from the language of the rule if 10-days includes weekends or is it 10 trading days. However, in either case, WWM failed.

Why it matters

Fair markets. Investors in public corporations own a share of the company. Those investors have a right to know who their partners are, especially those who purchase a percentage of ownership which may affect the direction of their company. Who the controlling owners are and their intent can materially impact the corporation and the stock price, as happened with Twitter this week. If someone like WWM fails to follow the regulations, it creates market distortions that benefit some investors and unjustly hurt others.

Additionally, it opens the possibility that the person purchasing more than 5% of a public company acquires shares at below-market prices for their benefit. Essentially, they are stealing money from people who may have unknowingly been selling shares in the company at a discounted price. Below is a calendar of WWM’s activities and the dates he skewed Twitter’s stock price.

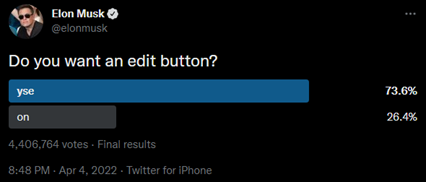

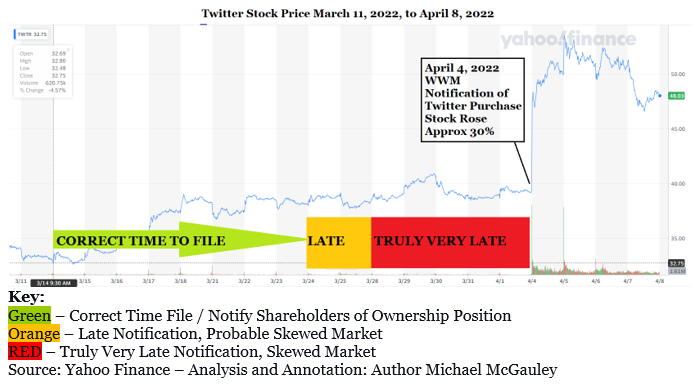

Now let’s look at Twitter’s stock price during this period. Within less than half an hour of when WWM notified the world, he purchased 9.2% of the company, the stock price launched in pre-market trading from the April 1 close of $39.31 to over $51 per share. A nearly 30% additional premium on a $31B unprofitable company makes it now a $41B unprofitable company. Adding an “edit” button won’t fix that problem, regardless of what WWM’s poll showed.

WWM’s April 4, 2022, Twitter Poll

Twitter shareholders and options calls had the opportunity to benefit from WWM’s shenanigans. Meanwhile, people who recently sold or held put options were hornswoggled and maybe defrauded due to the skewed market price.

Some people may claim the following. “So, the stock market price of Twitter was skewed for several days; who cares? It is a free country with free speech. Some people sold too soon. Nobody forced them to sell. They did so voluntarily. They would have made more money if they held their shares instead of selling them. Tough luck for them.”

The proper reply is, “this is why we have rules.” People agreed to participate in the market based on principles and regulations. Aren’t these compacts and covenants supposed to apply equally to all? For people cheerleading WWM’s Twitter Board appointment and company shakeup, consider if it was someone you truly despised instead of Technoking WWM. It would be equally wrong.

Who will pay for the market distortions WWM created? While typical SEC fines for late filings historically have been in the $100,000 range, the marketplace damage to participants is far more extensive.

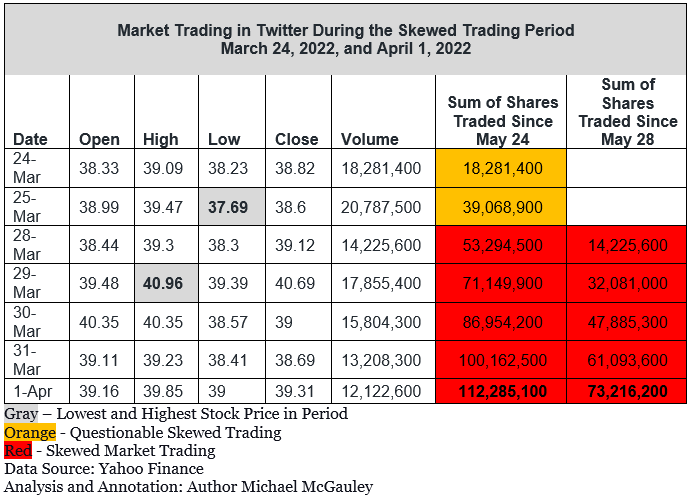

Below is a table showing Twitter shares’ trading volume and price for the dates in question. WWM released this information when he finally filed the correct 13D form notifying the market he intended to be an activist investor and become a member of Twitters Board. Strangely, WWM’s ownership went down to 9.1% of the company from 9.2% declared in WWM’s 13G notification one day prior. Was this an honest mistake or something else? Did WWM sell shares between his disclosures and violate the typical 3-day lockup period for trading shares post public notification? It’s not clear. Nothing in WWM’s filings explains this.

Given the above, skewed market trading of $2.7 billion ($37.69 times 73.2M shares traded) to $4.5 billion ($40.96 times 112.2M shares) occurred. That is a massive sum of money exchanged when market participants would otherwise have had additional knowledge about their company in normal circumstances and according to rules. Moreover, after you factor in options market distortions, the damages are assuredly even greater.

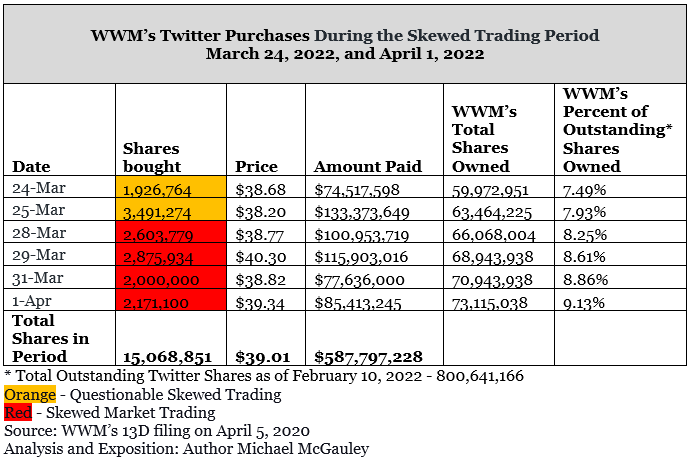

Additionally, WWM himself purchased shares in this skewed market. Below is a summary of WWM’s trades during the period.

Hence, WWM openly purchased over 15 million shares of stock in a willfully skewed market, of his creation, at an average price of $39.01. WWM spent $587,797,228 secretly purchasing these shares from unsuspecting, uninformed people, unaware that WWM was a significant shareholder in their company. It was no fault of their own; it was purpose deceit.

WWM didn’t care; after announcing his purchase, the value of just this batch of questionable shares rose to $752,990,484, given an approximate new per-share price of $50 based on the closing price of Twitter on April 1 of $49.97. WWM gained an astounding $165,193,256 additional net worth only by telling people he owned something. Not too bad of a week for WWM.

Howbeit, if you are one of the people who sold your shares to WWM, oh well, too bad for you. You and others lost $165M. You rightfully should have had the opportunity to make that money if WWM followed the rules. Maybe WWM will send you a check for the difference? Highly doubtful. Those people will have to seek justice another way; to recover their damages.

One can argue about potential efficiency improvements or ineffective regulations and penalties, but those are true of any large organization, public or private. Perhaps the SEC would agree additional improvements could be made, such as they have already done with the Whistleblower Program created by Congress in 2010. This program enhances the SEC’s ability to find fraud by enlisting public help.

One of the principal architects of the whistleblower program, Jordan A. Thomas, established the nation’s first whistleblower practice exclusively focused on violations of the federal securities laws. More recently, Joshua Mitts, a Columbia University professors research, contributed to a probe by the DOJ and the SEC into suspected trading manipulation. Hence, the SEC is constantly trying to improve its ability to fulfill its purpose. Every day many super-intelligent, industrious, committed, and assiduous people put everything they have into doing their jobs at the SEC and DOJ. These people have families, dreams, morals, and acting as public servants, they are trying to protect the rest of us while WWM flaunts them.

However, while one can debate and propose changes and improvements, one cannot intentionally create chaos and problems to be funny while costing other market participants money by manipulatively trading stocks against established rules and regulations to further their self-interests. We live in a Republic with free speech; we don’t live in a Plutocracy. Everyone can’t make their own rules and laws and pick and choose what to follow. One cannot commit fraud.

Our SEC and other public agencies have enough problems to deal with without intentional assailment, tomfoolery, and mockery by people who have the means to do the right thing and choose not to. However, we don’t live in an idyllic world, and people like WWM sometimes make life more challenging.

Believers in our great Republic have faith and confidence that society will collectively deal justice. It may take time, but many brilliant, honest, good-hearted people will not put up with people like WWM. Some of those people work at our SEC and DOJ. Sometimes life mirrors fables. As in Hans Christian Andersen’s king with no clothes, Technoking’s class clown masquerade may end with those laughing, not with him, but at him.

About the Author:

Michael McGauley is an activist investor and business consultant who filed his 13Ds timely and correctly. He is a graduate of Columbia University in Information and Knowledge Strategy. He enjoys working on high-impact matters requiring expertise, analysis, objectivity, and wisdom across multiple disciplines. Formerly, he worked with Ciena, a Fortune 1000 networking technology company. He led the management systems design for one of the largest telecommunications networks in the world. Road biking and indoor bouldering/wall climbing are two of his hobbies. Michael resides in the Greater Boston, MA, area. You can visit him at https://www.linkedin.com/in/michael-mcgauley/ or on Twitter (@mike_mcgauley).

Michael thanks Dean Chin for his assistance with editing this article.

Sources:

https://www.investor.gov/introduction-investing/investing-basics/role-sec

https://www.seclaw.com/can-the-sec-bring-criminal-charges

https://www.sec.gov/foia/docs/fulltimes.htm

https://www.investopedia.com/articles/07/secbeginning.asp

https://finance.yahoo.com/news/columbia-professor-became-scourge-activist-100856402.html

WWM’s 13G – 5%+ Ownership Declaration Filed April 4th, 2022 – at 06:04:17 (During pre-market trading)

https://www.sec.gov/Archives/edgar/data/1418091/000110465922042863/tm2211757d1_sc13d.htm

WWM’s 13D – Activist Investor Disclosure Filed April 5th, 2022 – at 17:18:39 (During after-hours trading)

https://www.sec.gov/Archives/edgar/data/0001418091/000110465922042863/tm2211757d1_sc13d.htm

Tesla Annual Report For the fiscal year ended December 31, 2021

The Vanguard Group – 10.29% Twitter ownership 13G filing April 8, 2022

https://www.sec.gov/Archives/edgar/data/1418091/000110465922044262/tv0013-twitterinc.htm

https://finance.yahoo.com/quote/TWTR?p=TWTR&.tsrc=fin-srch

LEGAL

© xdood LLC 2022